Your insurance company likely views mold as a maintenance issue rather than a structural emergency, even when it follows a catastrophic weather event. With water damage accounting for 22.6% of national homeowners insurance claims, the distinction between sudden damage and gradual neglect has never been more scrutinized. If you’re managing insurance claims for mold damage after a flood in 2026, you’re facing a National Flood Insurance Program (NFIP) that only covers mold if official restrictions prevented you from accessing the property. This technical barrier often leaves property owners vulnerable to significant financial loss and health risks from toxic spores.

We understand the pressure of facing a one-year filing deadline in states like Florida or navigating the 30-day response regulations in Oklahoma. You deserve a property that’s structurally sound and safe for habitation, not just a surface-level fix. This guide teaches you how to document damage with engineering precision, navigate the $1,000 to $10,000 coverage caps found in standard policies, and secure professional remediation. We’ll examine the current 2026 landscape of endorsements and explain why proving structural necessity is the only way to ensure a successful claim payout.

Key Takeaways

- Distinguish between “sudden and accidental” water discharge and rising floodwaters to determine whether your homeowners or flood insurance policy provides the necessary coverage.

- Secure your financial recovery by maintaining rigorous photographic evidence and mitigation logs required for successful insurance claims for mold damage after a flood.

- Understand the technical necessity of interior gutting to the structural shell, as surface-level cleaning often fails to meet long-term safety and air quality standards.

- Accelerate the recovery timeline by submitting an immediate Notice of Loss and utilizing independent abatement experts to establish a fact-based scope of work.

- Learn how integrating professional mold remediation with selective demolition prevents structural degradation and ensures your property remains safe for future habitation.

Navigating Homeowners vs. Flood Insurance Coverage for Mold

Determining liability for mold growth requires a precise understanding of your policy’s origin-of-loss definitions. Most policyholders mistakenly assume their standard homeowners policy provides comprehensive protection, yet these contracts specifically exclude damage from rising surface water. For Flood insurance, you must look to the National Flood Insurance Program (NFIP) or private market alternatives. Successfully managing insurance claims for mold damage after a flood depends on your ability to prove that the moisture source was sudden and that you took every “reasonable means” to mitigate the environment within the first 48 hours.

Standard homeowners policies operate on the “Sudden and Accidental” principle. If a pressurized pipe bursts on the second floor, the resulting mold is typically covered because the event was instantaneous and unforeseen. However, if the water entered from the ground up during a storm, the claim falls under flood insurance, which has much stricter mandates regarding mold remediation. You won’t find coverage for flood-related mold in a standard policy because insurers categorize rising water as a separate, specialized peril that requires its own contract.

The Sudden vs. Gradual Damage Distinction

Insurers prioritize the timeline of the event to differentiate between a covered loss and maintenance neglect. If moisture lingers because of a slow, undetected leak or high humidity, it’s classified as gradual damage, which is almost universally excluded. The burden of proof lies with the property owner to demonstrate that the mold isn’t a result of long-term structural oversight. Failure to initiate drying protocols within a 24 to 48 hour window often provides carriers with the technical grounds needed to deny a claim based on a lack of mitigation. Documentation must prove that the spores didn’t exist prior to the flood event to avoid the “maintenance neglect” clause.

When the NFIP Covers Mold Remediation

The NFIP, currently authorized through September 30, 2026, maintains a rigid stance on mold. Generally, it won’t pay for mold removal unless you can prove that you were legally or physically barred from the property by an authorized official. If a local government prevents residents from entering a flooded zone for several days, and mold develops during that period, the NFIP may cover the remediation costs within the $250,000 residential building limit. Coverage is typically granted only under these specific conditions:

- Official government restrictions prevented you from accessing the property to begin drying.

- The mold is a direct result of the flood and not pre-existing environmental conditions.

- The damage occurred despite the owner taking all reasonable steps to prevent growth once access was restored.

Property owners should verify if they have private flood insurance, which currently accounts for 35% of the Florida market as of February 2026, as these policies often offer more flexible mold riders. Without a specific endorsement, standard NFIP policies treat mold as a preventable condition, making immediate documentation and structural drying essential for any successful insurance claims for mold damage after a flood.

Essential Documentation to Prove Your Mold Claim

Securing a payout for insurance claims for mold damage after a flood requires a shift from anecdotal evidence to forensic data. While photos of standing water are necessary, they rarely suffice as proof of structural saturation. Insurers in 2026 employ sophisticated adjusters who look for any sign of pre-existing moisture issues to trigger “maintenance neglect” exclusions. You must build a comprehensive dossier that includes high-resolution imagery, professional moisture maps, and a minute-by-minute log of your mitigation efforts, such as the exact times industrial dehumidifiers or pumps were activated.

Organizing your documentation begins with a centralized file for all receipts related to temporary repairs and professional consultations. This includes invoices for initial water extraction and any structural assessments performed by certified firms. The Texas Department of Insurance emphasizes that maintaining a detailed record of communication with your carrier is just as vital as the physical evidence itself. Every phone call and email should be logged to ensure your timeline aligns with mandated reporting windows, which are strictly enforced at one year in jurisdictions like Florida as of 2026.

The 48-Hour Evidence Window

Mold spores can colonize wet surfaces within 24 to 48 hours, making the initial documentation phase critical. You should use a digital hygrometer to record humidity levels and an infrared camera to identify thermal anomalies behind drywall. These tools provide objective proof of “hidden” moisture that visual inspection misses. If you suspect saturation behind baseboards or within wall cavities, document these areas before they’re opened. Capturing the state of the structural shell before professional mold remediation begins prevents the insurer from claiming the damage occurred after the flood event ended.

Preparing the Proof of Loss Statement

The Proof of Loss statement is a formal document where you must categorize mold damage with technical accuracy. Avoid vague language like “the walls are moldy”; instead, use specific terms such as “microbial growth resulting from Category 3 water intrusion.” Third-party air quality reports serve as an essential validation of your claim, providing a baseline of spore counts that prove the environment is uninhabitable. Be careful with phrasing traps that suggest the damage was “gradual.” If your paperwork implies the moisture was present for weeks without action, you risk an immediate denial. Accurate documentation ensures the carrier recognizes the remediation as a structural necessity rather than a cosmetic preference.

Remediation vs. Structural Gutting: Maximizing Claim Value

Surface-level mold cleaning often fails to meet the rigorous safety standards required for permanent habitation after a flood event. Porous materials, including drywall, insulation, and carpeting, act as sponges for Category 3 floodwater, which typically contains pathogens and heavy silt. Attempting to scrub these surfaces only addresses the visible hyphae while leaving the root systems embedded deep within the material’s core. For insurance claims for mold damage after a flood to be fully realized, you must demonstrate that the contamination has compromised the structural integrity of these components. Payouts for extensive, whole-house remediation in 2026 often range from $10,000 to $30,000, reflecting the technical complexity of total contaminant removal compared to simple cosmetic wipes.

Stripping a property to its structural shell is a technical necessity when moisture levels in wall cavities remain above 16%. Professional hazardous material abatement ensures that the environment is truly stabilized before reconstruction begins. When insurers calculate payouts, they rely on the distinction between “cleanable” and “non-salvageable” assets. By proving that porous materials cannot be safely restored to a pre-loss condition, you shift the claim’s valuation from a minor cleaning allowance to a comprehensive structural replacement. This engineering-led approach prevents the recurrence of spores that often plague properties where only surface remediation was performed.

Identifying Hidden Contaminants

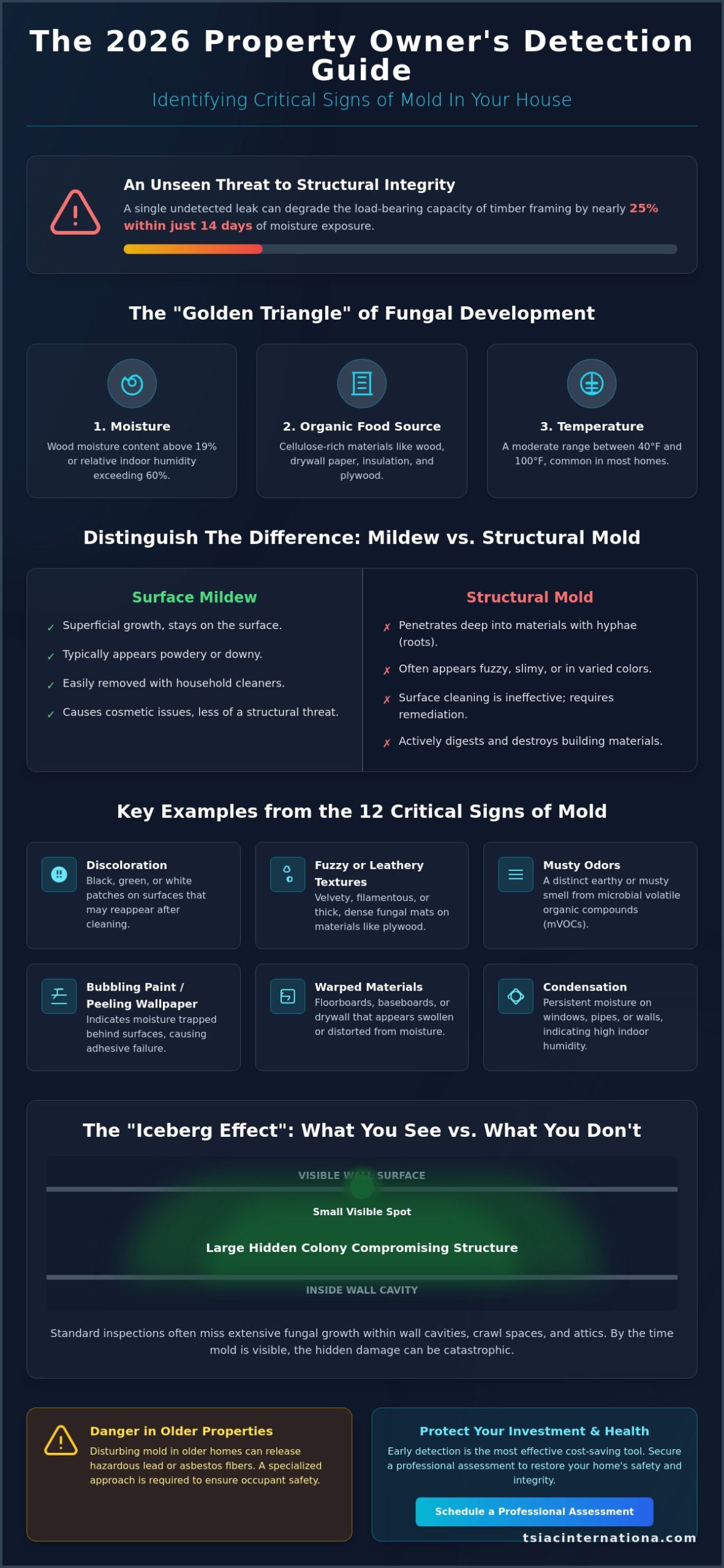

Flooding in older properties frequently disturbs legacy materials that require specialized handling. The saturation of walls often necessitates asbestos removal if floor tiles or insulation are compromised, as these materials become friable when disturbed during drying. Lead paint disturbance is another significant risk during flood-related gut-outs, particularly in structures built before 1978. A comprehensive abatement plan that identifies these hazards early simplifies the insurance adjustment process by providing a clear, regulatory-backed scope of work that adjusters cannot easily dispute.

The Case for Selective Demolition

Selective demolition is the surgical removal of specific building components to facilitate deep cleaning without compromising the building’s primary load-bearing elements. Gutting to the studs is the only method that guarantees 100% mold removal, as it allows for the direct treatment of the structural wood or metal framing. This process is a cost-saving measure for future structural integrity; it eliminates the risk of “sick building syndrome” and ensures that new drywall isn’t installed over a contaminated foundation. When managing insurance claims for mold damage after a flood, presenting a demolition plan focused on decontamination often secures a more realistic settlement that covers the true cost of a safe recovery.

How to File a Successful Mold Damage Claim Post-Flood

Initiating insurance claims for mold damage after a flood requires immediate technical precision rather than just a standard phone call. You must issue a formal “Notice of Loss” to your carrier the moment the water recedes. Under current 2026 regulations, states like Oklahoma now require insurers to accept or deny these claims within 30 days, making your initial reporting window tighter than ever. You aren’t just reporting a wet house; you’re documenting a structural failure that requires specialized intervention. Negotiating the scope of work between simple cleaning and full structural removal is the most critical phase of this process. If you require a professional assessment of your structure’s condition, the team at TSIA C International provides the engineering-grade insights needed to support your claim.

Handling the initial visit from the insurance adjuster requires a strategic approach. They’ll use standardized estimating software that often fails to account for the complexities of hazardous environments. You must be prepared to demonstrate why surface-level antimicrobial treatments won’t suffice for porous materials that have been submerged. Finalizing a settlement that covers professional remediation ensures you aren’t left with a “sick building” that loses its market value or structural integrity over time.

Initial Reporting and Mitigation

When describing the damage, use technical terminology that aligns with industry standards. Refer to the event as “microbial colonization resulting from Category 3 water intrusion” to underscore the health risks involved. Your policy mandates that you take “reasonable steps” to prevent further damage, such as running industrial dehumidifiers or extracting standing water. However, you must never discard saturated drywall, carpeting, or personal items before the adjuster has performed a physical inspection, as disposing of evidence can lead to an immediate claim denial. Maintaining the scene exactly as it was found provides the forensic proof required for a maximum payout.

Managing Professional Estimates

Relying on an adjuster’s estimate alone often leads to significant out-of-pocket expenses. A detailed quote from a demolition contractor is vital because it reflects the real-world costs of labor, disposal, and hazardous material containment. If the carrier’s plan is under-scoped, use this professional estimate to dispute their findings. Proving that the moisture levels in the wall studs exceed the 16% threshold for safe enclosure is often the leverage needed to move a claim from a “clean-only” status to a full interior gut-out.

When negotiating with your adjuster, focus on these three technical requirements:

- Present moisture mapping data that proves saturation deep within the structural shell.

- Challenge the use of “cleaning” allowances for non-salvageable porous materials like insulation.

- Demand a line-item breakdown for hazardous material disposal fees, which are often overlooked in standard estimates.

This data-driven approach ensures the settlement reflects the actual cost of restoring the property to a safe, structurally sound state. By treating the claim as a technical project rather than a simple repair, you protect both your health and your property’s long-term value.

Professional Abatement: Securing Your Property’s Future

Professional abatement represents the terminal phase of a successful property recovery strategy. While a general contractor focuses on the assembly of new materials, a certified abatement firm specializes in the forensic removal of biohazards and compromised structural elements. For insurance claims for mold damage after a flood, carriers require documented proof that the environment has been stabilized according to IICRC S520 standards. This restoration doesn’t happen through surface cleaning; it requires a systematic demolition process where saturated materials are extracted under strict negative pressure protocols. This ensures that as we remove mold-laden drywall or flooring, we aren’t inadvertently cross-contaminating unaffected zones of the structure.

Environmental compliance is a critical component of the recovery process that protects the property owner from future liability. Hazardous waste disposal must follow specific state and federal guidelines, particularly when floodwaters have mixed with industrial runoff or sewage. Once the interior is stripped to the structural shell, final clearance testing provides the empirical evidence needed to finalize the settlement. An independent industrial hygienist must verify that spore counts have reached baseline levels, providing the “safe to inhabit” certification that adjusters require to release the final portion of the claim funds.

The TSIAC Approach to Hazardous Remediation

Our methodology for interior gut-outs prioritizes engineering precision and rigorous containment. We utilize advanced HEPA filtration and physical barriers to isolate the work zone, ensuring the structural shell is completely decontaminated. With 15 years of experience in complex environments, we understand that professional project documentation is just as important as the physical labor. We maintain detailed logs of material removal and prioritize the recycling of metal framing and wood whenever possible. This disciplined approach provides the transparent record-keeping that insurance carriers demand for high-value insurance claims for mold damage after a flood.

Restoring Safety Through Expert Gutting

Stripping a building to its structural core after a toxic flood event is the only way to guarantee the long-term health of the inhabitants. By removing every layer of porous material, we eliminate the hidden pockets of moisture that lead to recurring microbial growth. This process prepares the site for a seamless transition to reconstruction, ensuring that new finishes are applied to a clean, dry, and verified foundation. Don’t settle for surface-level fixes that compromise your property’s value. Contact TSIAC International for a professional abatement and gut-out estimate to secure your building’s future.

Restoring Structural Safety and Financial Stability

Successfully managing insurance claims for mold damage after a flood requires a shift from simple cleanup to a disciplined engineering approach. We’ve established that proving structural saturation is the only way to move beyond restrictive coverage caps and secure a payout that reflects the true cost of recovery. By prioritizing moisture mapping and forensic documentation within the critical 48-hour window, you protect your property’s market value and your family’s health from the long-term risks of microbial colonization. Surface-level fixes aren’t enough when Category 3 water intrusion has compromised your building’s core.

True recovery is only possible when you strip the environment to its structural shell, ensuring every hidden spore is eliminated before reconstruction begins. At TSIA C International, we bring over 15 years of hazardous material abatement experience to every project. Our team is certified in asbestos and lead removal, specializing in the selective demolition required to stabilize complex sites. We don’t just clear the air; we secure the building’s future through meticulous abatement and technical precision. Let us provide the professional documentation and structural expertise your insurance carrier demands.

Get a Professional Abatement and Gut-Out Estimate from TSIAC International and ensure your property is restored to the highest safety standards. You’ve handled the crisis; let us handle the structural solution.

Frequently Asked Questions

Is mold always covered if it happens after a flood?

Mold is not universally covered and depends entirely on the origin of the water and your specific policy type. Standard homeowners insurance excludes mold resulting from rising surface water, while the National Flood Insurance Program (NFIP) only provides coverage if official restrictions prevented you from accessing the property to begin drying. If you have a private flood policy, which represents 35% of the Florida market as of 2026, you may have more flexible endorsements for microbial growth.

How long do I have to file a mold claim after a flood event?

The filing window varies by state and policy type, but you must act with extreme urgency. For example, Florida law requires that new property insurance claims be filed within one year of the date of loss. In Oklahoma, 2026 regulations now mandate that insurers accept or deny claims within 30 days, making it vital to submit your Notice of Loss immediately to trigger these consumer protections.

Can insurance deny my mold claim if I didn’t dry the area fast enough?

Insurance carriers frequently deny insurance claims for mold damage after a flood by citing “maintenance neglect” if mitigation didn’t begin within 48 hours. You’re contractually obligated to take reasonable steps to prevent further damage, such as water extraction or dehumidification. If an adjuster determines that the spores colonized because of a delay in your response rather than the flood itself, they’ll likely categorize the damage as preventable and exclude it from the payout.

Does flood insurance pay for professional mold testing and air quality reports?

Standard NFIP policies typically prioritize structural drying and debris removal over specialized testing unless it’s required to prove the environment is hazardous. Most homeowners insurance policies in 2026 cap mold-related costs between $1,000 and $10,000, which must cover both testing and remediation. You should review your policy riders to see if you’ve purchased additional endorsements for $25,000 or $50,000 that specifically include industrial hygiene reports.

What is the difference between mold remediation and a full interior gut-out?

Mold remediation often involves topical cleaning and antimicrobial applications, whereas a full interior gut-out is a structural process that removes all porous materials to the studs. Gutting is technically superior after a flood because it eliminates hidden contaminants trapped behind drywall or under subflooring that simple cleaning cannot reach. This method ensures the structural shell is 100% decontaminated before any new construction begins.

Should I hire a mold expert or a demolition contractor after a flood?

You should hire a specialized abatement firm that holds certifications in both hazardous material removal and selective demolition. A general demolition contractor might not have the equipment for spore containment, while a simple mold expert might lack the structural knowledge to safely gut a building. A firm with experience in asbestos and lead abatement provides the engineering precision needed to handle the complex layers of a flooded property.

What happens if my insurance adjuster misses hidden mold behind the walls?

If hidden mold is discovered after the initial inspection, you must file a supplemental claim supported by professional moisture mapping or thermal imaging. You shouldn’t sign a final release until you’ve verified that the structural cavities are dry, as moisture levels above 16% in wood studs will inevitably lead to recurring growth. Providing the adjuster with an independent estimate from an abatement specialist helps ensure these hidden risks are included in the original scope of work.

Will my policy cover asbestos removal if it’s found during mold remediation?

Asbestos removal is typically covered if the material was disturbed by the floodwater or if its removal is a prerequisite for mold remediation. Many policies include “Ordinance or Law” coverage, which pays for the increased cost of repairs required to meet current safety and environmental regulations. Because flood-soaked materials often become friable, professional abatement becomes a regulatory necessity that the insurer must address to restore the property to a safe state.